Live Music Archive

Live Music Archive Librivox Free Audio

Librivox Free Audio Metropolitan Museum

Metropolitan Museum Cleveland Museum of Art

Cleveland Museum of Art Internet Arcade

Internet Arcade Console Living Room

Console Living Room Books to Borrow

Books to Borrow Open Library

Open Library TV News

TV News Understanding 9/11

Understanding 9/11tv Capital News Today CSPAN October 30, 2012 11:00pm-2:00am EDT

11:00 pm

there is simply too much analysis. there certainly isn't opinion and i appreciate how i can really see through and understand the programming at golf and i can get my analysis elsewhere. if you want to see how your government works directly, c-span is the only place to go. >> until a few months ago, charles haldeman of freddie mac. he began the job in 2096 months after the company was taken over by the federal government. mr. haldeman spoke about the housing market and financial regulations at the john f. kennedy school of government. this is just under an hour.

11:01 pm

>> i'm a member of the faculty here at the kennedy school at a romani school of business and government. it's a pleasure to welcome all of you to this year's lecture, which is funded by nasd, which is now in the, the private broker of the u.s. industry. the focus is on financial regulation and each year we have had a leading public official responsible in some ways for u.s. regulation. this year, our speaker is a tiny bit of a stretch, but not really much at all. ed haldeman was ceo of freddie mac from a 2009 to just a few months ago. while in that role, ed was not really a formal regulator. he was responsible for running a very large public financial

11:02 pm

institution. freddie mac and its sibling, fannie mae are what are called government-sponsored entities, gics. for years described as private companies at the public mission of supporting housing or more simply, as mixed public-private enterprises. but in september 2008, both institutions failed financially. they were placed in government conservatorship, becoming quite unmixed just public corporations. the gics have had many problems of their conservatorship. ad was not part of that arriving by the year after conservatorship. but add was part of the solution. the risk of running freddie mac is a big challenge. it's very large business. about 5000 people. but the balance sheet at its peak, before conservatorship of just under a trillion dollars.

11:03 pm

that included about $800 billion of mortgages financed directly by friday and another $1.7 trillion of mortgages guaranteed off balance sheet. together with fannie mae, freddie mac's responsible for roughly half the u.s. mortgages made to homeowners. since conservatorship, the amount of mortgages directly on the balance sheet of fannie and freddie have declined, but their role in finance u.s. homeownership has in fact shot a. today, roughly three quarters of u.s. mortgages are made for her and she by freddie and fannie. i had a bit of a roll after his place in conservatorship yet i

11:04 pm

was in the freddie mac ford, head of governing and nominating committee. the first ceo of freddie was put in place by the treasury department at the time of conservatorship quit after six months. we had to make a pitch to add to take the job. it was fairly simple, and most challenging job, which is a germanic understatement. but the opportunity to do meaningful public service. setting for any needed strong leadership and steady guidance as they rehabilitated themselves and waited for the government to decide just what to do with them. i should point out that we are still waiting for the government to decide just what to do with them. it's now four years since the readership. and beyond some partisan back-and-forth about things handling of foreclosures, housing policy has been one of the elephants in the room during the campaign.

11:05 pm

ad has had an outstanding career in both public-private sector, leading important financial institutions after degrees from dartmouth, hbs and harvard law school and started his career with the philadelphia investment accounting film dealer. it was later bought i united asset management which churn for eventually ran he became the u. of delaware messman and next he was called to run putnam investments here in boston and even larger management firm that has advanced to the previous management. he righted that it eventually sold a good price for shareholders to a large canadian financial firm. it was at that time that we approached add to run. freddie and fannie, together with a broader issue of u.s. government involvement in

11:06 pm

housing finance is one of the major unfinished pieces of business and financial regulatory reform. it's clearly an important issue. we c-span here filming this. ed has the unique perspective. an experienced manager of the frontline running the gics and most thoughtful public policy participant. he's done when the talk about where the gics have been and what to do with them. my great pleasure to introduce ed haldeman. [applause] >> inc. so much for the kind introduction. i'm very appreciative of so many of you coming out tonight to visit with me and learn about freddie mac and the gics. i'm particularly pleased to be giving the glauber lecture here

11:07 pm

tonight. there are many, many people, perhaps hundreds, maybe even number in the thousands of people whose career was launched by bob glauber. i am one of those feared doctrine one-time investment management in 1973 at harvard business school and as he indicated, i spent approximately 35 years in the money management industry. so i don't distinguish myself based on my career been launched by bob glauber, but what i think it's a little bit special about me, perhaps unique is that my career began and ended with bob glauber. [laughter] is particularly this week, i think i have to be careful about the preposition i used in that last clause because rob was on the board. i was the ceo and the preposition i used was my career

11:08 pm

ended with bob, not by bob and i think it's a particularly insensitive to making sure everybody knows we ended our time at freddie mac together. i'm also pleased that the subject of the lecture tonight is freddie mac and the gse so i have an opportunity, now that i'm no longer the ceo, have an opportunity to present a balanced view of the gics. this is a subject, which i have come to see others speak very aggressively, emotionally. it is a subject he gets very heated and it is very uncommon for people to present a balanced view. in fact, my goal tonight is to present a balanced view and if i

11:09 pm

succeed, it may be the first time there's ever been a balanced presentation. certainly, the employees that work with me were passionate about the role, the function they perform, almost a religious kind of mission is what they felt they were doing at freddie mac. and it is hard to imagine that there were other people in societies that had the same kind of visceral feel in the opposite direction about the work that they did. neither side able to the the other point of view. hopefully in the course of the next 15 minutes or so, you will come to balanced opinion about freddie mac and the gics. i want to start with where they've been and go back quite a bit in time back to 1938, when the first gse was created,

11:10 pm

fannie mae, to think about what the mortgage market was late at that point in time because they think they're doing so, we'll see some of the advantages and good things that have been accomplished by cne, freddie and the gses. before fannie, the mortgage market was very different than it is today. the only thing available was short-term mortgages, five or 10 years, variable kinds of rates. the down payment on a 50% was the standard in those days. there is a payment at the end of the term. you had to, but the whole thing at the end of the short-term. very large variations with mortgage money and rate, no standardization, all done very locally with very different standards in the mortgage market was not at all connect it in as a result, rates were quite high in those days.

11:11 pm

subsequently, the mortgage market has changed radically and in large part because of ready, cne and the gses. most importantly, the mortgage market got hayley connected to the capital market, the secondary function performed by the gses connected the mortgage market to large pools of assets to the capital markets, including not just the u.s., but worldwide. there is standardization required by the gses, virtually an illumination of the variability in rates and liquidity by region. there was a broadening out in the access of mortgage money in our country before a very limited high income people very limited in terms of ethnic back down. the gses brought not a substantially and made sure there was white bread availability, fixed-rate, 30

11:12 pm

year mortgages. think about what is so special about mortgages and our country. today, for 3.5% interest rate, you can get dirtier money with no prepayment penalty, a pretty unusual economic opportunity. so those are the early years. the advantages the gses brought to the mortgage market. let's not think about the years just before the financial crisis and think about where the gses has been in that period of time. the reason is worthwhile taking a look at for the financial crisis is that there are many people who have argued in written at the gses cause the financial crisis or cause the great recession. as bob glauber indicated, i was

11:13 pm

not at freddie mac until way after the financial crisis, so i don't really have a stake in this game. but this is a chart i would look at too sore to determine extent i thought freddie mac, cne may cause the price is. i'm not saying that perhaps will find later some contribution, but do you think they cost it? this chart looks at market shares in the market share of the gses is at the top and it's up blue line. and then the british line that starts at the bottom and gets very high is the private market, so this is the investment banks in the commercial banks issuing secondary mds private-label securities we call them. look at the radical market share

11:14 pm

change. freddie and fannie going on the order of 75 or send down to 40%, falling like a rock. and the private-label taking tremendous share. but would be the cause of that? because in my view is a change in underwriting standards, a change from requiring substantial documentation and high underwriting standards, large down payment, many of the private capital competitors reduce some of the standards and were able to take substantial market share. now imagine you are the ceo of freddie mac at the bottom market share number, 40%. the senior market share go from 75% to 40%. he reacts not?

11:15 pm

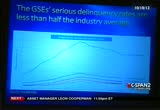

do you change your underwriting standards? how much can you tolerate in terms of market share loss? is the ceo of freddie mac at 5000 or 6000 employees. it looks like the entire market is going away from me. do i change not? i think the ceos, people running the company did make some changes and we each can make our judgment about what we would have done in that position, but at least argue it's a hard call. it would not be easy to be unchanged in terms of requirements on underwriting standards and have the market share go completely away like that. this is another indication of what i believe whether or not freddie was the cause of the financial crisis. and here we take a look at mortgage default rates over time

11:16 pm

the definition of default is 90 days to link went. you can see that i freddie and fannie at the wordstar delinquency rates cut up into the four to 5% down. for the overall market in our country, it got to be 10%. the subprime sector of the market he got into the 25%. so again, while i believe freddie and feeney did lower their standards, resulting delinquency rate, you can see a big difference between the way freddie and fannie behaved in the way the rest of the industry did. so where i come out en masse is

11:17 pm

that i don't believe that the two gses for the cause of the financial crisis. i do think they did produce underwriting standards, but i think i can understand why the ceo might have done not given what the competition was doing. i do think there were some mistakes and problems made that were connected to the gses and certainly one that i found troubling was summarized in about by gretchen morgenstern called reckless endangerment, which is the story of crony capitalism exhibited by the two gses. i view that look almost as a playbook on how businesses can execute crony capitalism and get close to government for their benefit, not just an incredible lobbying organization, not just

11:18 pm

campaign contributions, but things like hiring repeatedly people coming out of government, opening regional offices and all the critical congressional offices and hiring relatives of congressmen in order to fill those regional offices. so to be sure they offered is accurate. a second problem was the implied government guarantee. this is not some lame but necessarily was generated by the gses, but rather took advantage of it. but what they were able to do because of the implied government currently was fire essentially as much money as they wanted to at the government rate. so unlike most private companies, when you put on more

11:19 pm

and more death as the rate goes up, they were able to borrow almost unlimited amounts of the government rate and then create a retained portfolio, which some people described as a hedge fund because one is able to arbitrage the difference between the government rate and the rate they use to buy in some cases private-label securities. so i don't think the gses for a halt, but i do think it is a stretch to call them the cause of the financial crisis. so let's talk about what the gses have done subsequent to the crisis since they put into conservatorship to point in time that i'm more familiar with. one of the things they have done in one of the reasons i took the job is that they have been the

11:20 pm

only game in town for the mortgage market. and here, the numbers accounting for 75% of the total mortgage market if you add in fha, another government mortgage provider commuted to about 95%. so the private market has been providing only 5% of the mortgage money. where would we have been over the past three or four years without the gses performing this function? in addition, we worked with the administration in treasury department in order to execute some of the government programs. home affordable modification program and home affordable refinance program. you can see the number of modifications done since conservatorship is 1.2 million homes, a big number.

11:21 pm

the only problem is when the idea of modifications was first generated. the program was quickly taken over by political people in and close to the white house and they decided they needed to make an announcement about what hamp was going to do and they said it was going to do three or four modifications. i've no idea how no one got the number, but someone wanted a big number as result, 1.2 has always seemed like it wasn't very successful. it's a pretty big number and the gses executed not just the modification program, but also the refinance program. one of the things we didn't do was we didn't do principal forgiveness and that is -- a not quite ready for this one, but on this list of things up here, we

11:22 pm

didn't do principal forgiveness in some of you have read criticism about us not doing we didn't do principal forgiveness and some of you have read criticism about us not doing. we believe pretty strongly as some of you have read criticism about us not doing. we believe pretty strongly as did our regulator that there was a real risk of strategic default where we offer a program of principal forgiveness, which is to say that even though freddy has lots of underwater mortgages , over 80% are still current. nobody had any problem or has continued to make their obligation despite being underwater. we worried about principal forgiveness having some impact on those a cent of the underwater mortgages and we thought it's better to focus our attention on hamp rather than add principal forgiveness. i wanted to spend just a minute on another part of our

11:23 pm

subsequent conservatorship, which would be profitability. many of you have read about standing back and freddie may. in front of you is two bars. one is the amount to draw with taken from the federal government and the green bar is a moment dividends paid. what a lot of people don't recognize is that the dividends that we have to pay now i remember like $7.2 billion a year. so if you generated $7 million in income, you'd still have to draw something from the government and that's why people continue to talk about draw. if you look at the total record for the entire time, the round numbers rhr from the government of 70 billion dividends at 20 billion, beating a net drop of 50. you can see them to designate

11:24 pm

when that your son come, the draw was 40 billion. so everything subsequent to 2008 has been a drive required to pay dividends. that is a net neutral impact on the treasury. and the reason we been able to get to that level of profitability is that all the mortgages that have been put on in the last years during conservatorship have been very high-quality in terms of down payment and in terms fica score, much higher than was the case prior to conservatorship. this new book, besides subsequent to conservatorship now accounts for 60% of the total primark. so that was all passed. we talked about the real old time. come on 19 we took a look at the pre-crisis. a much that post-conservatorship. let's now look forward and think about what to do with freddie

11:25 pm

mac going forward. it has been a great frustration to me that the treasury department and the administration has come up with no program policy recommendations as to what to do. it is now 50 months we've been in conservatorship. it's now 50 months to 6000 people who work at freddie mac don't know if the company existed no job security at all. the treasure was to put out a position paper in january 2010 with the subjective solution. they didn't do that. it didn't come until january january 2011 and then the white paper of the stooges three options, three options obvious to anyone on day one of conservatorship. so it's a great frustration remained a progress in this area, particularly when i believe there is strong consensus on what we ought to do.

11:26 pm

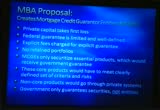

before you is a proposal put forward in august of 2009 by the mortgage bankers association, which talks about farming companies, friday capital companies they call it the cheese, market credit guarantee entities, which would be three to five the number of the private capital companies to compete with one another, that there would be no government guarantee of the companies. there'd be a government guarantee of the securities, mortgage back securities. or for that t., they would pay an insurance premium much like fdic insurance. the securitization would only be a plain-vanilla kind of mortgages. anything outside it would have to be done in the private capital market and there would

11:27 pm

be no retained portfolio at all. so we had this proposal, a sensible proposal in my view in august of 09. three years later, a really smart guy named jim milstein who is at the treasury department, the guy was possible for the restructuring of aig is the voyeur in investment in keene restructuring kind of person and he put out a proposal, which has many common ingredients that we saw from the mortgage bankers association. here, the emphasis is on a government agency. the federal mortgage insurance association, which authorizes management regulate a series of securitate there's the issue mortgage-backed securities and again, the company are not guaranteed, just security czar.

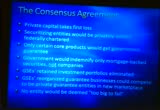

11:28 pm

the beauty of both of these proposals is that the technology in the infrastructure and system in the human capital of the gses would not be reset, that could form the basis of one of these securitize theirs to compete in the private capital market going forward. so i believe that there has been some consensus around a proposal that is feasible would work. one was issued by somebody who had an ax to. that is the mortgage association, but milstein coming from the treasury department come up or simply his view is what is best for the economy, but it's a very similar proposal in my estimation and i wish that we could move ahead with them being like this then you would be tremendous benefit icing for the taxpayers to get some usefulness out of this investment that they have made

11:29 pm

in the gses and keeping them together and functioning, to use the skeleton, to use the infrastructure and awaited that allows the taxpayer to get a benefit, to get some monetization of the investment that is then made over time. ..

11:30 pm

>> i have made my decision to leave freddie mac because i thought it was going to take a long time before we would get resolution. unfortunately, i joined the

11:31 pm

company the middle of 2009. at that point, everyone was certain that the company would be relaunched at some point. possibly in a couple of years. obviously, we have been disappointed in that. as the calendar rolled through three or four years, i concluded looking at my birth certificate that i probably wasn't going to make it. that was one indication of my pessimism about when we were going to get this resolved. it was clear to all of us that as we got into the election year, that nobody was going to spend any time on it, and it has been remarkable how the candidates have been on the subject, given how much of it we

11:32 pm

have talked about. significant things like tax policy and policies on deficits. i think there is going to be a long period of time before we will get any action on this. i'm just talking about when someone puts out an idea, which has to be challenged in congress and debated, and then you get something fast, and then you have the implementation. after all, think about where we are as far as implementation in terms of obamacare. unfortunately, i am very pessimistic about when we finally get resolution. >> yes, sir. >> i am a student at harvard kennedy school. you started your remarks talking about the incredible remarks

11:33 pm

before the conservatorship. as we think about the entities that will follow, how we think about creating an appropriate amount of political installation against lobbying when it comes to capital requirements or appropriately pricing governments guarantee? >> that is a real important question. i can tell you that during my time in the conservatorship. we had really strong restrictions. we were not able to make any political contributions. not just the corporate level, but i, personally, was not able to do it. i happened to go through law school with a couple of senators. i was not able to visit with them even on a personal sense. it precluded from any interactions.

11:34 pm

we had to go to a regulator. initially, all the lobbying and the lobbying people were let go. i can tell you that it has been totally insulated with a couple of exceptions, which were really annoying to me. which member of congress, who felt like they own freddie mac, like they own me, but they would call on my personal cell phone. i don't know how they got it, trying to make me intercede on some action the company was about to take. presumably a foreclosure can kind of activity that have gone

11:35 pm

through the process. it was asked to intercede. there was an attempt in that direction. all of that makes me a little bit pessimistic about your question. i think when we get to the resolution, one would hope that we would have the private capital company, which would be regulated very closely with restrictions on campaign contributions, lobbying, those kinds of things. but we are also going to have to have strong leadership for those who don't buckle to the pressures that they receive. but it is a problem. i guess against the reason that i'm not too pessimistic is because we have gone through this period of time where we have been incredibly disciplined about employment and political

11:36 pm

activity. >> you also talked about the discipline of the gse during this period. what they have guaranteed. have you come money pressure? >> very modest. obviously, the statements made by members of the treasury department administration suggesting that we were too tight or the other place that we would get a little bit of pressure is how aggressively we took the push backs to financial institutions. the very modest and reasonable, i would say, not particularly troubling. >> okay. >> hello, i am a student here.

11:37 pm

i really like your charts. it looks that we focus on the single-family side of things, and i'm interested to see about what to think about the multi-family aspect. >> thank you for that remember to grab a supporter. this is the second time i have spoken since the vice presidential debate, and as a result, every time i sip some water, i wonder whether it is too much or too little or whether it is appropriate or not. [laughter] >> so multi-family is a really great story. it is about 20% -- excuse me, 10% of our business, but it is a successful business. it is one where we have had -- i showed you where we are no matter what time period we are looking at.

11:38 pm

there was a default rate, such that many people but that can be spun out and that is a -- another way taxpayers could receive money. i'm very proud of the efforts that we have made in analyzing multi-family. i think that it could be a very successful standalone company. going forward. >> hello. i am asking this question on behalf of the jfk junior reform committee. would you say that the companies

11:39 pm

have lost the ability to recapitalize themselves? >> i think in the traditional way of using the word recapitalize themselves, yes. because of the 10% dividend requirement. when most got institutions to have bail out, there was a 5% dividend with an ability to repay that. freddie and fannie, the dividend was 10% with no ability to repay. as a result of that, the ability to recapitalize themselves, to use your phrase, really isn't fair. and the numbers for freddie mac is like $72 billion, meaning that the dividends payments annually at 7.2%.

11:40 pm

it is really hard to generate enough capital to meet that dividend and accumulate on your balance sheet. you have a chance to recapitalization. >> i am the senior at the college here. thank you so much for taking the time. you begin your talk by discussing the important advances in the mortgage market after the introduction of gse is. i wanted to know in your opinion and looking forward, to what extent do you think a more purely private area is able to or would be able to achieve the public polls of the gse? >> okay, let's hypothesize no government involvement. you'll remember that i had

11:41 pm

limited government involvement, none of which are too big to fail, none of them have a government guarantee, but the mortgage-backed securities that they issued would be government guaranteed and there would be an insurance premium paid for that guarantee. that is the extent of the government. let's hypothesize to go to your question that there is no ultimate reinsurance, ultimate backing of the security. the disadvantages to that, i think, would be largely in the cost of mortgages. i believe that the mortgage rates would be materially higher as compared to my suggestion. and the reason is that i think that there are big sources of capital worldwide that will only

11:42 pm

invest in our housing mortgage market. if there is some kind of ultimate government backstop. i think there are big pools of assets in asia, for example, that will only invest if there is an ultimate government backstop. i visited during my tenure with some of the holders of freddie mac security from foreign institutions. and they said they would not buy anymore and we would reduce the holdings, because even under the current state of affairs, they were not exactly comfortable with the ultimate government guarantee. we made it clear how significant was to have that guarantee. big pools of assets in our housing market. for that reason, i am willing to tolerate a limited amount.

11:43 pm

>> without government involvement, it would be a higher price for mortgages. and i bet that is right. but the consequence consequence would be a higher mortgage, of course. what would be the consequences of that. would it be good, bad, or not either? >> the consequences of higher rates? >> just. >> well, i think that they would be significant. i think that already, we are going to narrow down the universe of possible homebuyers. because the down payment is so

11:44 pm

large and if you compound that with a higher interest rate, you will narrow that potential home buyer down to a level which i think is unacceptable in american society. and we definitely went too far towards the goal of making everybody a homeowner. we had that single-minded objective of getting that percentage higher and higher, and i think that we push too hard. but i think that if you compound a 20% down payment with significantly higher mortgage rates, i think we would be marrying the universe of homebuyers into small groups. >> my name is jacob and i'm a sophomore here at the college. i wonder if you could talk about the climate and culture when you assumed leadership in 2009.

11:45 pm

what were the expectations and pressures? >> yes, i am trying to describe a little bit. so there are five or 6000 people that work at this company. many of them, like people employed anywhere in our society had in invested a lot of their money in the company. the 401ks, stock holdings. many people are proud of the company that they worked for, and they bought stock in the company. their holdings went down to zero. i am not saying everyone had 100% of a 401k, but there were big holdings that went to zero. and then the people were criticized by politicians as

11:46 pm

being the cause of the financial crisis. these are people doing great work helping people. many of the employees told me that when they would wear a freddie mac t-shirt or sweatshirt to the supermarket or the home depot, they would be accosted by people. acosta for what they had done. as bob indicated, they were put in the conservatorship. six months after the ceo arrived he left. two months after he left, the person who was a chief financial officer, age 42, took his own life. he didn't do anything -- there was no fraudulent activity, but because of the stress. so the employees had that list

11:47 pm

of thoughts and pressures with no job security or idea whether the company was going to exist. remember that there were senior politicians who repeatedly told the press that freddie mac should be abolished. in the paper that the treasury put out, they said many times that the company should be ground down. that is what the friends of the gse said. imagine the morale of the people because of that i try to spend as much time as i could being visible in talking to them and trying to come up with hope for the future. which was around this notion of us getting ready in some form to

11:48 pm

relaunch the company. the good news is that people hung in there and they continue to work hard. they are continuing to function quite well. >> hello, my name is josh, i am a student here at the kennedy the kennedy school. i want to ask you for your perspective on -- or your perspective on the book faultlines. it talks about the need for cycle group regulation. he observes that we come up with these great ideas. ideas like you articulated very well. they get this number, political pressures are applied to what he calls credit populism. seeing that we need to figure out ways to build regulation that somehow that won't happen. they are immune to those

11:49 pm

pressures. any thoughts on how we can do that? >> no, it is a great thought. only partially facetious, one of the best ways i know to prevent many who have been in this situation before. builds and builds and builds, and people become more and more aggressive as things go up and

11:50 pm

up. and then they reverse themselves. it seems like a new generation needs to go through that for they believe it. i think experience and people -- having people on staff, the regulatory authorities or companies who have gone through a few cycles is one great thing to have there. then i think that trying to insulate regulators from the political process is really an important thing to do. we certainly did not do that right at the gse. you can see there was an attempt made to take the teeth out of the regulator. they got too aggressive. they call people on the hill to intervene. those are two thoughts that i

11:51 pm

have on how you might be able to accomplish that goal be mapped okay, we have to end, so let me take one last question. scott, i am a stock member here the kennedy school. thank you very much for your talk. a question on the campaign. you said that there is a proposal from the treasury in terms of what to do next with the gse is. and presumably, an obama administration would follow something along those lines after dealing with the fiscal cliff and tax reform and all the other issues that are on the agenda. what about romney administration? what sorts of proposal, if any, have been articulated? >> well, let me make it clear that i did not say that there had been a proposal by the administration. they produced a long awaited white paper in january of 2011.

11:52 pm

a government solution, he plans solution, or a hybrid solution. i am not being facetious in saying that. so we haven't had a proposal from either side. the mortgage market has changed because of that and i think that the republicans and the administration, as they came in, would want to go more towards a free-market kind of solution without any gse. i would hope that the suggestion that i made and the mortgage bankers association made would

11:53 pm

be seen as something that both sides could live with, and that it is largely a private capital solution. there is not a freddie or fannie. they're our are capital companies that are competing to have the ability to pay a premium in order to get a government guarantee of their underlying security. i would hope that that would seem is enough of a free-market solution that republicans would be okay with it. and enough of a protection of the housing market that the democrat folks might find it acceptable. >> okay. thank you. >> thank you. [applause] [applause]

11:54 pm

>> even the story the textbooks left out, real people in american history, very important moment in american history that we don't know about. the first pilgrims in america came 50 years before the mayflower. they were french. they made wine. they had the good sense to land in florida in june instead of december in massachusetts. but then they were wiped out by the spanish. we let this story out of the textbooks. the most famous woman in america, she was taken captive by indians in 1695. up in new hampshire. in the middle of the night, she killed her captor and realized that scalp him, she's got them, and then she went back to boston as a heroine. they actually erected a statue to her. a first statue of a woman, an american, chewing a hatchet in one hand and the scalp in the other. >> we will take your calls, e-mails, and tweets in india.

11:55 pm

watch live at noon eastern on both tv on c-span2. you are watching c-span2 with politics and public affairs weekdays featuring live coverage of the u.s. senate. on weeknights, watch key public policy events, and every weekend, the latest nonfiction authors and books on booktv. you can see programs and get our schedules at her websites, and you can join in the conversation on social media sites. >> a former general partner of goldman sachs spoke to students at roger williams university in bristol, rhode island, last month. mr. leon cooperman start his own hedge fund in 1991. his company, omega advisers, it is valued at $5.6 billion. leicester team made news for accusing president obama of

11:56 pm

class warfare against investors. >> good afternoon. good afternoon. glad you are here. my name is jerry dauterive. i would like to welcome you to our distinguished leader presentation. we are very glad to hear you and have you here. c-span is taking. i ask that you turn off your cell phones. i would like to thank you for joining us today. our president and vice president is here of the company. i would also like to indicate

11:57 pm

that charles haldeman was our distinguished leader and speaker. it is great that also mario can join us to honor his friend, leon cooperman. we go back a long ways. our speaker last year is here to help us welcome leon cooperman campus. he and mario are legends. i heard it on cnbc, so i know it can be true.

11:58 pm

mr. cooperman has been in the investment and financial industry for a long time. he is the president of the new york society security analysts. he said earlier today that people talk about him, but he doesn't care for, but he needs to. not only is he a leader in the world of finance, he is also a leader in the world of philanthropy. i was reading an article from "the wall street journal" about him. and it was entitled, giving others a chance of the american dream. he talked in that article about he feels that he lived the american dream and he has devoted a good part of his life to giving others the opportunity to pursue the american dream. he and his wife are from the

11:59 pm

giving pledge, a commitment started by warren buffett and bill gates. they give away a majority of the wealth to charity. he is a longtime donor to the columbia business school. he is the recipient of the american jewish committee humanitarian award. the boys and girls club of newark, new jersey, and again, you know, he is a real leader in both fields. he has a bachelors degree from hunter college business school. and he is an honorary doctorate from rutgers university. it is my pleasure to welcome leon cooperman. [applause]

12:00 am

>> thank you for the gracious introduction. i think i'm going to keep the reserve for my obituary. [laughter] >> it is my pleasure to be here. mario delivers. it is the essence of a good friendship. i have found over the years that exceptions like these are valuable to you as the quality of your questions. i would be happy to respond in the areas you'd like me to develop my thoughts on. as the cover sheet shows, i'm talking about life, hedge funds, the investment outlook.

12:01 am

given my diverse background, i will respond to your questions from a number of vantage points. i'm a kid from the bronx that became successful so i could speak to the issue of being poor and being rich and that is an easy one -- which is better. [laughter] >> second, i have been a research analyst. i have been a pontificator, and a manager of the organization for the past 20 years. i can speak to being in the brokerage business selling research services to people and on the buy side. there thirdly, i was a director

12:02 am

of the processing for 20 years. i can speak to the issues of corporate governance. and also lastly, i have had a philosophic involvement. really, it has been a great trip for me from humble beginnings. my god, may he rest in peace, was a plumber in the south bronx. very similar. i have to put mario in the humble category. i was the first generation born in the country of america. mario's grandfather died in the cool mind in 1890s and he was born in america. mario is equally successful and deserves all the success. but i think in describing a trip from the south bronx to hear, i should be an inspiration to all

12:03 am

of you. i say this with great sincerity. with an average iq, strong work ethic and a heavy dose of good luck, you can go very far. i started my journey going to public school in the south bronx. i then went to high school in the cell phones. given my skills and language, i would probably still be nonwhite. i'm probably still have a problem with english. upon graduating from hunter, i worked for 18 months at the xerox corporation. in return to columbia business school where he got an mba and open the door to wall street.

12:04 am

my first observation is whether it was right or wrong, getting an advanced degree to improve my credentials, open the door to wall street, and i'm sure, goldman sachs, probably not recruiting a guy my level, so that mba open the door to goldman sachs for me. i, myself, prefer a phd, but that would stand for poor, hungry, and driven, because i get to learn from their parents. ever since it was introduced into the marketplace, i have used -- i used it this morning, a men's cologne called obsession by calvin klein. frankly, that is the word i would describe to describe my approach to the business.

12:05 am

a shorthand translation would be the harder i work, the luckier i got. i would say that hard work has never killed anybody. and i think to be successful in your chosen field of endeavor, be prepared to achieve that success. when the sun comes up, it doesn't matter who you are, but you hit the ground running. in my industry, roughly speaking, if you allow me to round off, 10,000 mutual funds,

12:06 am

many which are managed, 1% or less, let's say, roughly 10,000 hedge funds that request variation of 1% or 2% and 20% of the profits in the enumeration. assume for the moment that your clients are fools and ours aren't. we have some of the most sophisticated clients. if it is like this, they basically think you are outperformed. you figure out what to do and the market is underperforming.

12:07 am

if you want to get paid more, no resting on your laurels. you have to work harder. you're probably in the wrong business if you have second thoughts. these are some of the elements of philosophy that i have. but they don't want to share them with you. it took me 45 years to develop this glossary. i see a lot of young nice faces in the audience and i want to impart this to you in your careers. andrew carnegie center on 1900 that i wish to have in my epitaph, okay. one of the secrets to success is to surround yourself with the most able and capable people and don't be threatened by them. but be benefited by them.

12:08 am

within my career, have been very fortunate to have, in my service, men and women that made me better than i was. and i was able to hold onto them because i properly share the fruits of the labors. it is important to have the quality people on your side. so i share the benefits of my business with people. those that work with me. my personal philosophy of life i summed up four years ago when i took my entire family at that time -- i had two sons, 46 years old and 43 years old. my two daughter-in-law's. at that time, two grandchildren. i took them all away for an all expenses paid vacation to a hotel. and i explained to them that a male human who is surviving to

12:09 am

age 62, will typically live to age 85. the good news is that i'm doing well, but the bad news is i have lived a great deal of my life investing. i gave up four observations about life that i've get to you. that is, number one, there's nothing more important than family. they root for you and care about you the most. stay close to your family. under all circumstances. second, i really consider mario one of my great friends. it is great to have friends, but to have friends, you have to know how to be be a friend. extenders cell phone every time. be trusted and supported. in the words of ralph waldo emerson, the only way to have a friend is to be one. that is very important in life. third, i told my kids, never do anything in life that you would

12:10 am

be embarrassed about that appeared on the front of "the new york times." finally, when you are the chief financial security officer, share with others less fortunate than yourself. in the biblical sense, we are at a moral obligation to help others in need. i have read a lot of words of other people that struck me in a manner that impressed me better than words that i could make up. i use the words of others. i don't know any of these people, by the way. i knew henry ford, but not any of the others. the first test of a gentleman is to respect those that cannot be of any possible value to him. i have seen people over the years -- those who treat those in a superior position to them

12:11 am

very nicely better and nasty to people that are no value to them. i detest that kind of behavior. my view, respect people no matter what they can do for you. whether they are above human life or below you. people deserve respect and dignity. they will come back and report you in many ways. henry ford said that the best way to make money in a business is not to think too much about making it. warren buffett, who is a contemporary, one that mario and i have great respect for, he said go to work for the people you respect. don't worry about the money. everything else will take care of itself. you know, we all economic people to a degree. but i think it's very good advice. be with people you respect and admire and don't worry about money and hopefully the rest will take care of itself. william ward, i thought his

12:12 am

words were very insistent and i believe in his words. before you speak, please listen. before you write, then. before you spend, earn money. before you invest, investigate. i do that most of the time. before you criticize, wait. before you upgrade to forgive, before you quit trying, before you die, dead. that is a very good sequence of advice. i have a granddaughter that is poetic and she just turned 14. she had been writing and came back from two weeks in santa fe, new mexico. an educational two weeks for a child.

12:13 am

[inaudible] >> if you are not for others, no one will be for you. if you are for others, you will be for you. now or never. i would say the relevancy to you, because giving is probably not something you can afford to do now. you are in a competitive world today. one of the things you should do is hopefully you want to add your own initiatives. at a minimum to improve your stance in the world is to try to find community activities that you can get back to to distinguish your resume from the next person. it is people like me are getting resumes every day in this difficult economic environment.

12:14 am

from high class standing people. 800 sats, they are looking for jobs. what you have to do is find a hook on your resume and show a high sense of community service. when i interview people, basically, the desire and commitment to be the best, a strong work ethic. here i am introducing a legend. you know, the legends do

12:15 am

something different. you know, these are some of the characteristics. you can get help from the university. if numbers don't speak to you, in other words, ben graham wrote a book called the intelligent investor in 1954. in the bookie prophesies that analysts evaluate management twice in the process. once through the numbers. when you look at a company, the company is growing and the return investment is widespread and profit margins and whatever -- the return to capital and whatever -- those are resulting from the efforts imagine. so you want to look at the financials. also, you want to look at the face-to-face and understand the business properly.

12:16 am

if you don't like working with numbers and people, my guess is that the area of security analysis might not be that appealing to you. i found a tremendous amount of interest in the hedge fund industry over the last five or six years. i want you to know that it is not a one-way street. this is an article written in "fortune" magazine in 1970 and 1971 by a distinguished writer named carol. she writes a lot of the annual reports for warren buffett. she couldn't have been more wrong. this article is written to rein in the death knoll for the hedge fund industry after the 68 and 70 market. if you look at this, everyone

12:17 am

has been really beat up. okay? but today, i could name is the hedge funds that are over $10 billion. so the argument that the industry was over was totally wrong. it is a little bit like darwinism, right? survival of the fittest. what separates the men from the boys is the diversity and how you deal with it. the last 20 years, i had investors, you lose a certain

12:18 am

amount of self-esteem is the environment waves, but i always buy my way all out of the hole and come back. and let me talk to you about this. looking at the economy and interest rates, i'm going to try to talk about everything and let the q&a drill down to where you're most interested. we are in equity hedge fund with macro capabilities. macro being bonds, currencies, commodities. we have a management $6.6 billion. about 14 in our firm.

12:19 am

we try to make money from investors in five different ways. no one way is more important than the other way. the five ways we make money on number one, market direction. i don't care how smart you are, we spend a lot of time studying the economy, the fed, market valuation, and trying to determine whether stock markets are going up or going down.

12:20 am

number one, we do a lot of work in the area of allocation. we look at stocks versus bonds. and with bombs we look at government bonds versus industrial bonds. high-yield bonds, and structured corporate credit. we are trying constantly in canada and western europe. what we are trying to find is a straw hat in the winter. during the winter, people do not buy a straw hats. they buy them in the summer. so it could be potentially undervalued. third, we like to spend the bulk of my own personal time on the long side. we visit companies, we knock on doors. we study industry statistics. we study valuation. we try to determine whether stock is misplaced.

12:21 am

we buy it if we think it is undervalued. we wait for the market to recognize what we think we will recognize. then we move on to the next undervalued security. fourthly, we distinguish a hedge fund from a mutual fund or it and it takes two things. an egregious structure. most managed from 1% or less. hedge funds are similar to this and get a percentage. the other thing that establishes them as you can sell stock short. if you sell something you don't own because you think it is overvalued, it declines in price. we do a certain amount of macro investing where we might have a view of interest rates that we have -- long or short bonds. we can do that with oil. the economy is slowing, there

12:22 am

could be an extra supply from the price could drop to $80. the idea of buying it at $80, we might buy that 100 because we think it will do well at $120 for it can be currency or commodity and it could be bonds. 13.5%, all the fees to the investor. at 100 points in excess of s&p 500. we have done not that with an average position of about 70%. we are less than fully invested and we returned the excess of the market. now gets more difficult. when we talk about the investment outlook. now gets more difficult. when we talk about the investment outlook. i am really kind of added information stock because i've

12:23 am

been very optimistic the last 2.5 years. but i'm beginning to become a bit optimistic. rather than specific forecast, i would like to show you my methodology. some of the things i am looking at don't resonate. again, i should tell you something about the right career path to consider. some can tell you more about the forecast in the future. i have mentioned that the 6.6 billion that we manage, roughly a quarter of that is the capital of the partners of the firm. warren buffett popularizes his notion that he eats his own cooking. if we lose money, we lose more than anyone loses because of the investment and we make more -- we make more than anyone makes because of our investment. in a sense, we have a complete

12:24 am

alignment of interest. we live in exciting times. but i have to say that the message i'm giving people now, every forecast or market view is based upon certain assumptions. let me tell you what monarch or that i will develop my views in more detail and statistical substantiation. my first assumption as the economy continues to grow, albeit slow subpar rate at about 2%, and that we don't fall into recession. that is very important. almost every recession is preceded by a bear market. if we don't have a recession, the likelihood of a bear market is small. secondly, and this is taking a

12:25 am

lot of brainpower and people. and that is the ecb, the european central bank, continues to stabilize the command in europe and the fed itself in the united states. and the eurozone governments, particularly germany, acts in a cooperative way to fund a weak european sovereign debt. further, the european banks raise the course of the capital they have to raise. and the ecb takes off troubled loans and they earn money with a positive yield slow curve. the european financial institutions are earning their way out of the hole. let me just say that there have been two schools of thought. one school of thought has been

12:26 am

that the problem is so complex, so difficult to understand that it exceeds one bandwidth then they don't want to invest. the second school of thought, which i perceive would be 45 years and investing, everybody believes that it generally doesn't hit. so maybe it was an wasn't easy way out. what i have been saying is that the breakup of the year awards eurozone, the ecb, the imf, 70% funded by the united states, germany, france, japan, will all chip in to do what they have to do to kick the can down the road. and we will not have a catastrophic outcome in europe. it is still my belief.

12:27 am

when people start to think more about them on those ways, if you listen to what germany is saying today, compared to what they were saying a year ago, it is totally different. the euro breaks apart, and they stock trading separate currency, they will go to the swiss franc were germany cannot export anything competitively. it is important to keep the eurozone together. in the united states we have one central bank. it is more difficult to bring everyone together. the third assumption i'm making is being challenged right now. the chinese are in the midst of a soft landing, not a hard landing. we will have growth between six and 7%. you know, that has to be watched very carefully. the chinese government, i think, is in the stages of significant easing. they cannot afford a significant economic slowdown.

12:28 am

because of the potential for social unrest in the country. the best way to think about the problems is simple. 800 million farmers and we'll need 200 million farmers. many people have to have employment. if they don't have employment coming of social unrest. the biggest challenge the government there has defined, jobs for 25 million more people every year. that is what they are working on. so the principal conclusion is driven by these authorizations and all my discussions that follow, which justified the statements. okay, the conclusion that i have is it is not clear whether it is a good or bad neighbor, and i still believe that, by the way. the first thing, let's talk about the economy.

12:29 am

a picture is worth 1000 words. basically, as you can see from the little column, the average economic expansion, when one gets going, basically is lasting about five years. sixty months. whether this expansion could be longer or shorter than average, if i had to debate that, i would argue that it might likely be longer than average. so many sectors of the economy are still operating below potential come and given the severity of the recession of 2008. so we are starting to come back below demand. housing is way depressed and below a normalized demand. ..

12:30 am

there's still pent up demand the consumer sector. the conservative financial poverty, housing starts way below normal ice demand. i won't read every one of these that juries, but these are reasons why we stand before you, expect dean economic growth to continue. our economic remark is on this exhibit. were expecting something between two and 2.5% growth and

12:31 am

basically it's not a feel-good environment, but nonetheless, it's an environment of growth. the reason i say it's not a feel-good environment and you should understand the statistics, it in the u.s. economy, typically the labor force by people seeking employment grows about 1% a year. the productivity of the labor force grows about 2% a year, so you need about 3% growth in real terms to make a dad or even keep unemployment level. we're not growing up that route. we're or going on a sluggish, subpar root. you can argue different reasons and at the house in order given the size of the budget deficits. the uncertainty that exists over the fiscal close and the tax regime and antibusiness policies and practice by sun.

12:32 am

whatever the case may be a committee economy is growing, but not a feel-good economy because the growth is not rapid enough to reduce unemployment and economy. giving users import, very important to both the consumer and consumer psychology is housing. you see really ingredients for a decent sized recovery in housing activity. affordability is near record high. home prices to disposable income is running your buckled low levels, so houses are cheap. in fact, the value of a home is a functional is a functional is a functional is a functional. rents have gone up relative to house prices in its now cheaper to buy than to matter. people have not been doing that aggressively because one of the most important expenditures as a home purchase. to the extent they are not

12:33 am

confident to home prices have bottomed out, they don't want to make that jump, that leap. as the search is the evidence come to pass prices out come the back the bidding contest in neil beamer to mistake. homeownership has declined to very low levels. rent mortgage payment is at record high. again, it's not cheaper to buy than rent. you see existing home prices starting to rise. voter confidence is rising anheuser inventory and all this excess inventory has been absorbed. i think it's an important underpinning of the economy. secondarily, we talk about the fat. when mary and i came to wall street 45 years ago, there is a trite, but correct statement. that was the central bank or federal reserve word wrote the market letter for wall street.

12:34 am

when the fed was tightening canoeists restrict it. negative the market and the fantasies he is positive. the central banks all over the world are telling you they want more growth, are willing to risk more inflation. they want more employment and attracting interest rates down to relatively noncompetitive levels. so you look at my supply growth exploded over the last couple years. the federal reserve balance sheet is exploded as they taken books that the banks to get the banks more ability to lend to the private sector. retailing with the federal funds rate that has been seared now for a couple years and recently fed chairman bernanke spoke and how about the prospect that interest rates remain in the short embassy row for a couple more years. now the ecb balance sheet as a percentage of gdp. the brink of the koran lic.

12:35 am

central banks all over the world, china is in very early stages and that's got to be positively. another common sense way of explaining that, and i'll try to remember not to repeat myself, but basically all of us in this audience to varying degrees have a challenge of investing financial assets. some have little, go to school and get an education. some have more. what are your choices today? choices are basically cache, which is zero. u.s. government bonds which i discussed his 1.5, 1.6%. negative return after inflation. high yield bonds i'll show you in a little while there repriced others common stocks as you go through the next few minutes, you'll see why they're in the financial asset neighborhood. very, very important to any

12:36 am

value investor is where you're getting into the market. you could be very right on your stock pick, the running entry point and not make any money. so i try to give you the market versus historical days. for the last 50 years and 2010, the s&p average about 15 times, 14.9. in that period of time the average of 14.9, the u.s. government on come into the right after 6.67%. well, here we are at the markets about 13.5 times the estimates of earnings, roughly 10% below the average for the u.s. government bond of 1.6% is almost a quarter of the long-term average. so interest rates are quite low, extraordinarily low. when the inflation rate in the country range between 1% 3%, it's close to 17. as i look at this exhibit against the span of time, stocks

12:37 am

are cheap against history, very cheap against interest rate and very cheap against inflation. i think the stock market is suggesting and it's probably a good suggestion to look at higher interest rate over the next two years as our economic growth versus history. but the extent that it's been discounted as discount for conservative consumptions. i'll give you a parallel. to the year 2000, the last bubble intact allergy shots. in 2000 from a selling at 100 times our assessment of earnings. it had no dividends commenced at the yield was zero and u.s. government on racer 6.5%. fast forward 12 years today, cisco is 10 times the estimate of earnings. the stock yields 3% versus zero and governments are 6.5.

12:38 am

so you can now buy it are incorporation that yields twice the 10 year government bonds are yielding in the multiple that's one 10th of what it was 12 years ago. said the valuation looks appealing. i don't believe the returns will be fabulous going forward as historical numbers brought forward. whatever you prodded the told 14 times earnings where you are now, they returned one year later with 15%, three years later 16% and five years later average 15%. so we are fine and historical context, where returns prospectively are very tracked it for reasons i'll discuss later, there's always the dark side for everything. i think the terms are nearly as attractive historically going forward. i mention that stocks the end of best financial asset. i find the chart very interesting. at omega we made a great deal of

12:39 am

money in 2010, 2011 and part of this year the high yield bond market. as you look at the bloomberg chart, november 2008 was a once-in-a-lifetime, i hope because the suffering and pain you go through this. so dramatic you don't want to live through it again. it safely was once in a generation opportunity in high-heeled or the high-yield market was 25%. even the senior securities to come in at nearly 25%. the equity market was 10% pst by senior security yielding 2.5 times what the equity market has been. if you look the bottom footnote, i find. when the high-yield index is 25%, the s&p multiple was 13.9. the high-yield index is now sub 7% in the multiple market not materially different than two

12:40 am

dozen eight. delegate to a cyclical peak earnings. but nonetheless, the high-yield bond is about a quarter peak coming at the multiple market is not substantially different when high yield was four times greater. anyone who follows the high-yield market will take credit spreads are historically very tight and yields are historically very, very low. that wants in a generation opportunity is gone. then mary and i always had a favorite professor that shaped and nurtured her interest in security analysis, professor roger murray at columbia. i could remember like it was yesterday. 45 years ago we told the class of 1950 eight was the same this year the market. they went on to explain 1950 year at the yield reversal. prior to 1958, stocks yielded more than bonds. we were coming out of world war ii, there is a great fear of post-world war ii recession, depression, let down in the

12:41 am

beginning of 1958, when people thought the economy growing and companies going end up being that the store and its suburbs virtually every week, the market brought in the concept of total return. they returned to stock is not just a dividend, but a dividend coupled with the growth of the dividend. well, we turn back over 50 years of history. as you can see from this chart, when i put this together, over half the stocks now yield more than bonds. government bonds are artificially depressed by the fed, you know, policies. but this is higher than it was in 2008, which is 45% and looks back over the years that they like we are now. you can buy many, many stocks in a hope your best input managing money, which he knows will never get back where the other money of the university and your investment club activities that

12:42 am

she seen many, many stocks yielding an access of arms and these are growing companies. now i was probably somewhat inappropriately quoted. i should arrive late. i was correctly quoted, but i said it would be caught dead using the u.s. government on the net not outlandish statement. it's a correct statement by the way, but too strong. what better method saturday questioned the u.s. government's ability to pay us back. they'll pay you back, but you're just not been compensated for the risk. so i thought it incumbent upon me to explain my position. historically if you look at the 10 year u.s. government on come the yield mind with nominal gdp. nominal gdp is the summation of real growth and inflation. so if you say to yourself that the world would have been would be something like 2% to 3% real

12:43 am

growth in 2% to 3% inflation, that means nominal topline gdp look at company sales heard somewhere between 4% and 6%. keep in mind that 4% were not going to absorb more unemployed people, so there'll be social policy tilted to generating more economic growth. well, if history repeats itself in the 10 year government bond goes back to nominal gdp, that means in a few years time when we get out of this economy, the government bumblebee 4%, 5% or 6%. well, this is bond arithmetic. a train ticket the second time. if we go for 1.5 to four in three years, including the coupon, you've lost 11% of your money. he lost 16% of your money because it goes to 20% of your money. maximum loss of tax they is 35%.

12:44 am

if you buy a bond of 1.5%, you'd leave the state taxes and you really can after tax return of 1%. doesn't wash. i think the capital is being confiscated. i've no particular interest in government bonds as an alternative common stock. now the last area i want to mention kind of comes in the world of contrary opinion. you know, is an expression for the city to come to wall street will come to respect and understand and that is the stock market does whatever's got to do compound the largest group of investments. what never was complacent and comfortable the forecast for guys like me come in the market is something that surprises you. in the last five years have seen a significant tea risking by the public and by institutions of the equity ownership. so what would the pantry be? the market goes up because everybody is expecting the market to go down. so you look here and see a band,

12:45 am

every year in the last five years comes to get selling of equity funds by the public. what are they doing? they buy bond funds. even though the market is up 14% to 15%, but continuing to liquidate. then you look at the pension fund set to appear pension funds go from 60% to near 50. most of actuary assumptions in the pension minus 7% or 8% a year. if either can be real estate private equity or equity is. and many lecture at the public. they've gone from 29% of financial assets in equities down to around 20 in the holding stock funds in decline and bond funds raised in you so i say the pantry to the public as if the market were not and not going down. now, i don't understand here in front of you and appear like the village because i'm not.

12:46 am

the economy faces a significant number of issues that we have to deal with. one is the so-called fiscal cliff. if nothing happens, there's legislated tax increase in expenditure cuts that the economy of $576,000 which is a little bit less than 4% gdp. if we have a gridlock in government, they don't want to talk to each other, they'll negotiate, we can only series that back. i refuse to believe that it appeared at the end of the day the same group didn't like each other and to decimate, but they did do in terms of legislation to get the economy out of a sharp dive. so rather than push us into a dramatic recession that they'll be compromised as, but it's not 100% clear that it's going to happen. so i think there's something we

12:47 am

have to kind of think about and worry about. i have a firm view about the coming election. we can talk about that later in q&a, but that's a personal opinion. it's like talking about abortion. a lot of people with different opinions. i'm very concerned about the huge buildup of federal debt. the commonsense observation of the nation was founded in 177,616,000,000,000,000 federal debt. we went from 2012 to 16 trillion. the up by a trillion dollars a year. it's unsustainable. we have to do with this. the commission some symbols came up with credible ideas, but would do nothing with them. unless we move in this area, it's going to be a significant issue. and while were not greece, we could have similar type problems. not to the same degree of freedom of sergio with problems as you can see this happening to debt relative to the size of the economy. that's the problem.

12:48 am

lastly, there's huge legislated tax increases on the horizon, not particularly friendly towards capital formation. the current tax rate dividends are% out i guess you can see right there 15 f. obama has this way, almost tripling the dividend tax increase. it's going to be about 50% or so increase the tax-free capital gains. if you love or the tax tax return on investing, you're basically going to love her the amount of investment taking place. so we have to resolve issues, which basically confront us and probably nothing's going to happen until november 6 received a leader of the country and who controls congress. these are factors we have to worry about. now my observation was to go back early into my career.

12:49 am

i say that what the big smile and certain sense of modesty, but i got my mba from columbia in january 311967. fas child was at business school for six months old when i graduated. i had no money in the bank like national defense education and student loans to repay. so i'm sure you've learned if you have liability no asset to make it if not worse. i hope you are not an basically had no choice but to go to work immediately. the very next day, february 1st 1967 i thought of my goldman sachs. on february 1st 1967, the dallas roughly 850. lo and behold, 15 years later was it okay. and i made my money by flying things that were very cheap.

12:50 am

so our 700 of the doubt, equivalent. even though the old world market was going nowhere. i can very well appreciated scenario for the cause in need of government around the world to get the financial house in order of the next two years we can remain in environment at see we deal with the fiscal cliff, as we deal with the huge deficit issues in the market and sees a need to deal an intelligent fashion. so unprepared. you folks are young, early 20s, late teens, whatever tissue can muster another three years for this. as i said at the beginning life expectancy is 82. another three years is going to be very painful to me, but i'm going to do it. i'm going to work out of because this what i love doing and have an obligation to do. i took somebody's money and effort to manage it intelligently improperly.

12:51 am

i'm a value investor. some of her versus what is a investor meeting? what it means to me as i want more for less. so when you look at the stock market, basically the s&p 500 is an index to 500 companies. on average across about 5%. on average it's usually about 2%. it's about two times book value of the companies in the index. but that's about 80% of its capital. debt-to-equity plus dead. the returns on equity currently is about 16%. normally it's closer to 14 or 15. and the ratio for that is just a cold galoshes 13.5 times. as a value investor looking for companies growing more rapidly and sevilla were multiple or have more dividend yield on the market at a lower valuation would maybe give me a lot more asset value versus the value i am paying for.

12:52 am

so you could be value invested by apple computer. apple is $120 billion in cash. 12.5 earnings, all the equity capital in the balance sheet. if you have the outgrowth, won't be like us than the last few years, but i think of a 20 the next few years. since growing four times the market. you have to accept technology risk. don't forget three years ago we are standing here talking about where were going to get her thumbs on the black very and now black or subscriber in the united states of america is dropping at a rate of 2%. they do not doubt. i joined xerox out at hunter college, my first job basically was all about american photocopy. you don't hear about them anymore. when the world of technology, someone's obsolete, so you have to make the judgment call. it's what he thought of. it looks for more for less. i said at the outset that i was

12:53 am

becoming a little bit less sanguine. sometimes you're in the midst of changing the view, adjusting of even speaking at the time and you need more time to think things through. firstly, the market now at the lovely tattoo is about 13.5 times earnings. but if any operand of the range in the market of the last three years. seth at the upper end of the range the last three years. the third quarter this year, the third quarter this year will be the first down quarter year after year since the third quarter of 2009. so the rate of increase in corporate profits actually could very well be down for a while and that's a factor. as we get closer and closer to the end of the year, the fiscal cliff issue amongst larger and there's huge uncertainty regarding tax policy that they mentioned before. i first said china is going with

12:54 am

the next acted and has to be watched very, very carefully. finally, the ecb while they take important steps, there's a lot more things regarding fiscal integration, big set to union and stuff like that. so i think we, you know, i think i've adjusted ourselves now to level a fair evaluation. personally the markets got 5% up from the 10% down, but i intend to follow the advice of the professor teaching phd's at columbia and one of the students upon graduation went to the professor said professor burns committee of any bias that i'm graduating? right now i'd say i tried to develop the reasoning why. i think near-term as much risk in the market is reward, but i do believe properly select the company maybe cooperman, we can

12:55 am

make money in the market. i hope i have touched on things that interest you. i'd lock in long-term money aside access to public markets because i think interest rates are a generation must be if they don't belong here. we look at fiscal condition of the country and our plane on the u.s. economy continuing to grow at a modest pace. it's always a student getting ready to go out to pursue my career, it's just get the best education you can come of the best grade you can come to get back to community service, try to distinguish a resume for the next person because you're in a very good live environments and you have to strengthen your credentials to every extent you can. i'm going to start. take questions. [applause] >> thank you. we have time for only a couple questions because mr. cooperman

12:56 am

has to be a mystery to see a screen. if he doesn't get it about five minutes he has to drive to new jersey. i don't want to do that. >> dismissed the jury? who are these guys? >> i'm a student from roger once. first question. you put a lot of a monstrous fundamental analysis about an intrinsic value of companies and they set off for the fair market value. what are some key indicators dbase is often how much reliance you put towards behavioral analysis? >> output of reliance in my ba view. i'm very analytical. 19 darius matos m. revenues, costs, earnings, and growth rates, market position and growth the market, so on and so forth. we have a certain view of what the growth rate is worth.

12:57 am

if it is selling, grand hypothesize that if her security had to be an intrinsic value. the job of the security analysts is to recommend securities of basically selling below intrinsic eye as a result of grocery returns, cash flow generation. most important is free cash flow. there is nothing -- they have no luxury of pursuing alternatives. with the free cash flow they can invest in business, buyback equity and pay dividends. that's the elixir that keeps things going. most important in the good industry, with honest management. i would not knowingly invest if someone was dishonest. i've invested knowingly within, to people because something was just too cheap to ignore. more often than not, you wake up with fleas, but i'm a little bit like warren buffett accepted out about lacey rose in the sense

12:58 am

that he believes in investing the well-run come to me. in fact, his favorite expression was he like to invest in companies be managed by an because sooner or later he'd be running them. it's pretty humorous and no one caught that one. are there to invest in businesses that are cash flow generators, run by capable management, with the management is properly incentivize to do the heavy lifting and benefit from their hard work. so the best case in point, it's rare for manhattan and was an investor with workshare hathaway for 50 years and that of the partnership and kept his investment of berkshire hathaway. i think is right for a bill in a billion dollars. the essence of investing, find the well-run come to me, make sure it's properly compensated and benefit from this

12:59 am